Discrete Choice and Random Utility Models

PyCon Ireland

11/11/23

McFadden and BART

“Transport projects involve sinking money in expensive capital investments, which have a long life and wide repercussions. There is no escape from the attempt both to estimate the demand for their services over twenty or thirty years and to assess their repercussions on the economy as a whole.” - Denys Munby, Transport, 1968 ”

Revealed Preference and Predicting Demand

Self Centred Utility Maximisers?

- The assumption of revealed preference theory is that if a person chooses A over B then their latent subjective utility for A is greater than for B.

- Survey data estimated about 15% of users would adopt the newly introduced BART system. McFadden’s random utility model estimated 6%.

- He was right.

- Copernican Shift: He estimated utility to predict choice, rather than infer utility from stated choice.

Note on Model Evaluation

Replicating the Super Soldier Program

Note on Model Evaluation

Replicating the Super Soldier Program

The Problem: Interpreting the Model

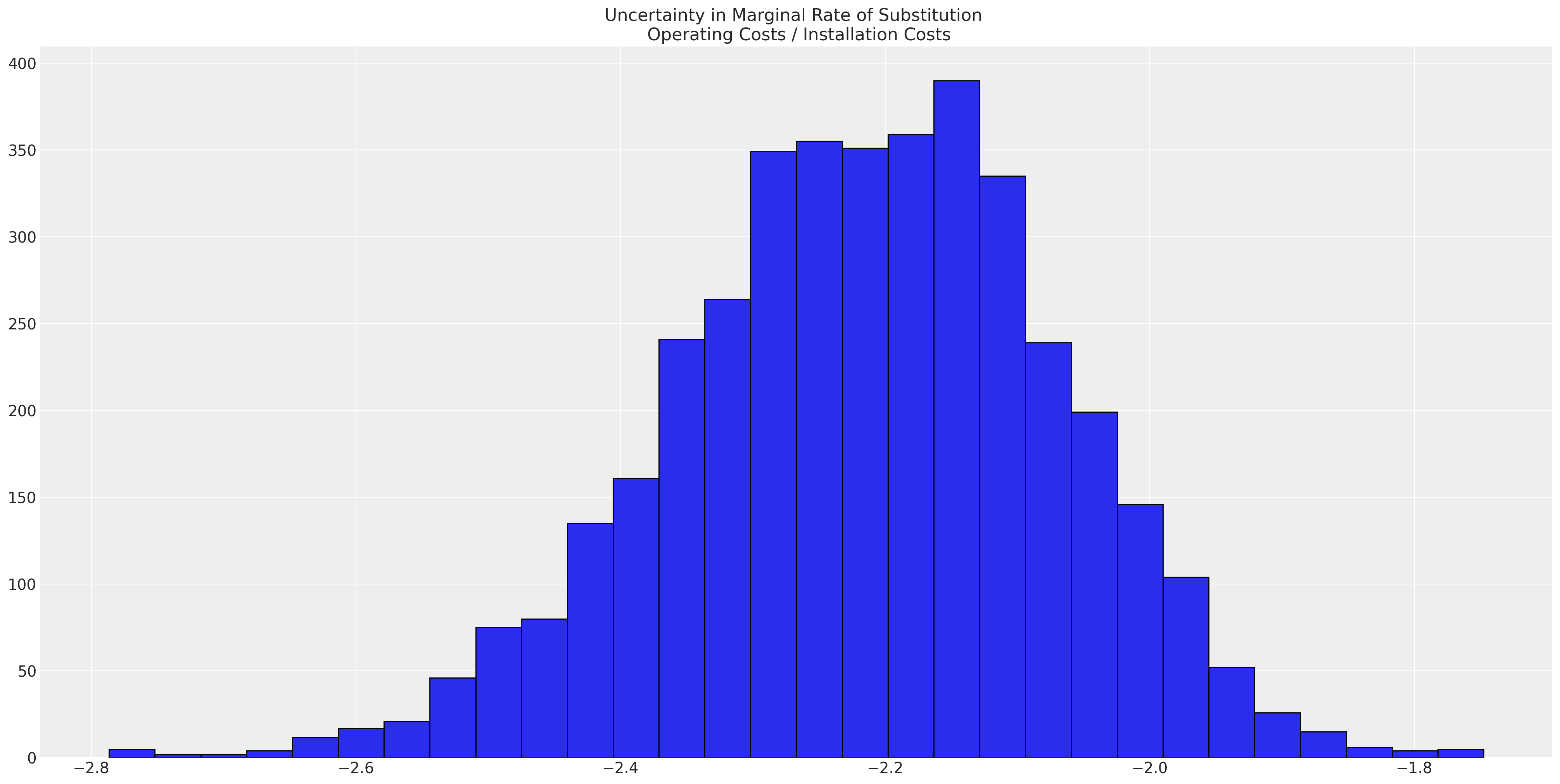

Rate of Substitution

The beta coefficients in the model are interpreted as weights of utility. However, the precision in these latent terms is relative to the variance of unobserved factors.

The utility scale is not fixed, but the ratio \(\frac{\beta_{ic}}{\beta_{oc}}\) is invariant.

The Problem: Model Structure:

The Process of Bayesian Updating calibrates the parameter estimates against the data

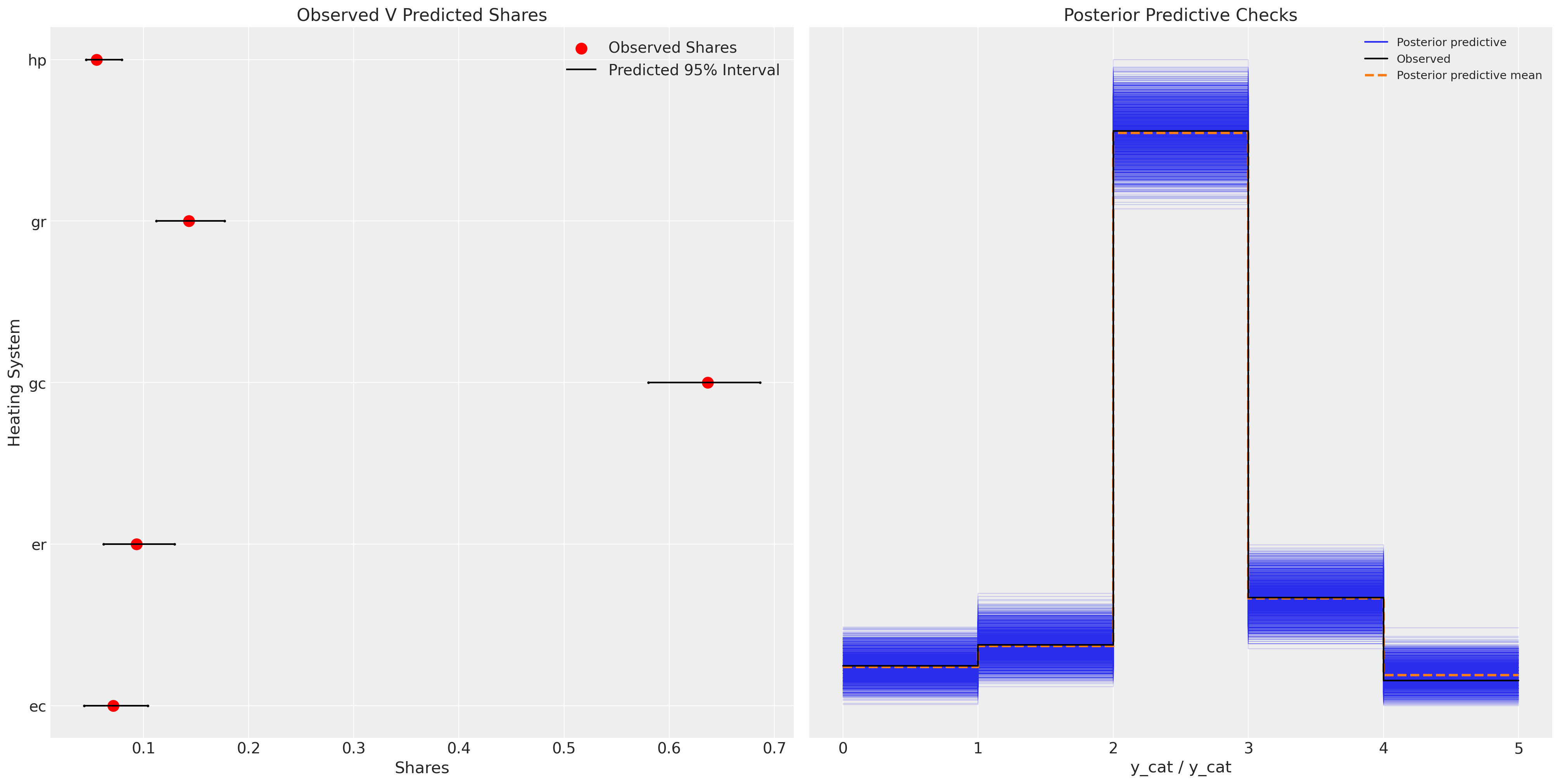

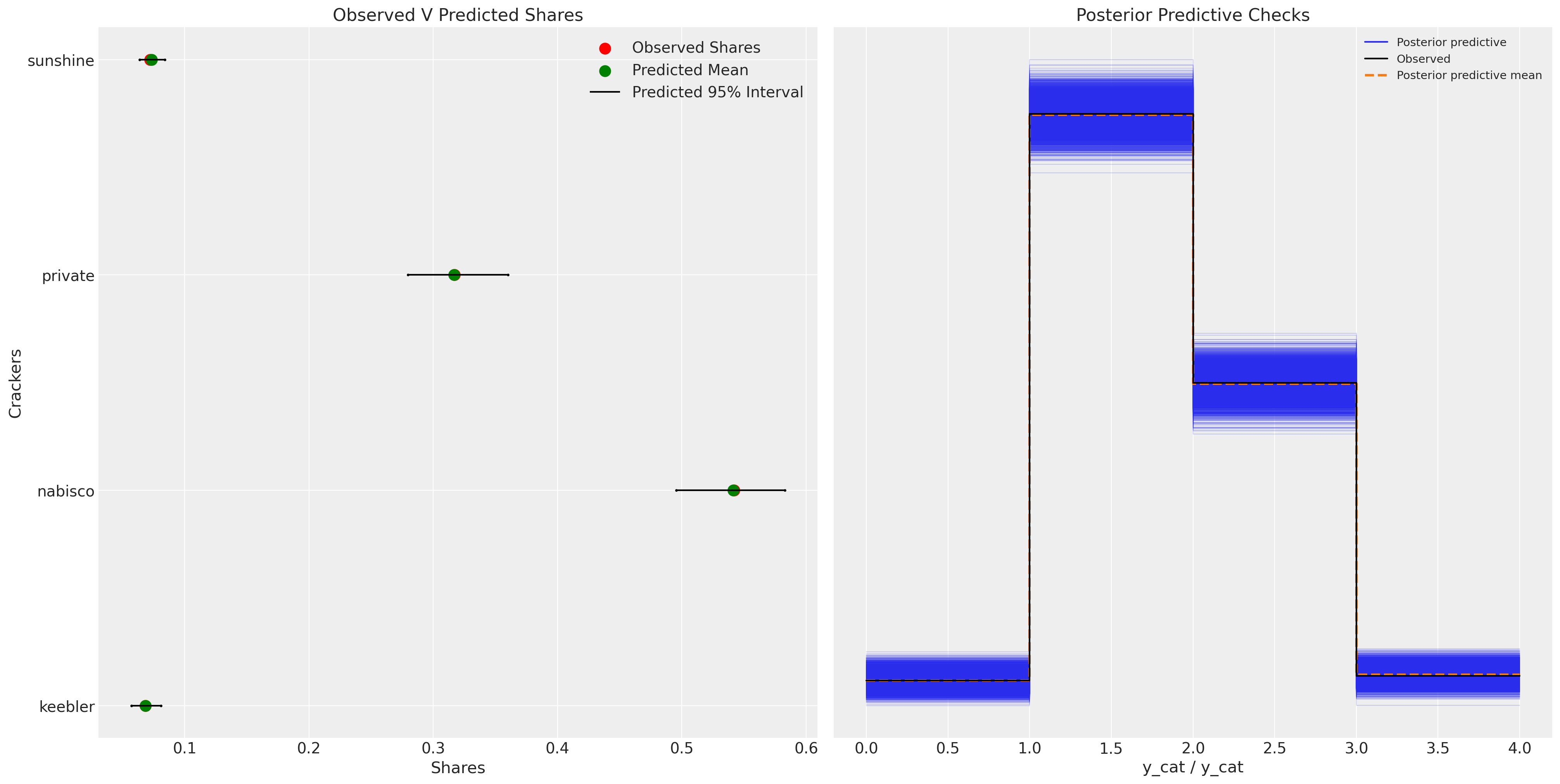

The Problem: Model Fit

Posterior Predictive Distribution

The model successfully predicts observed market share

Adding Correlation Structure

Structural Dependence

Correlation Structure

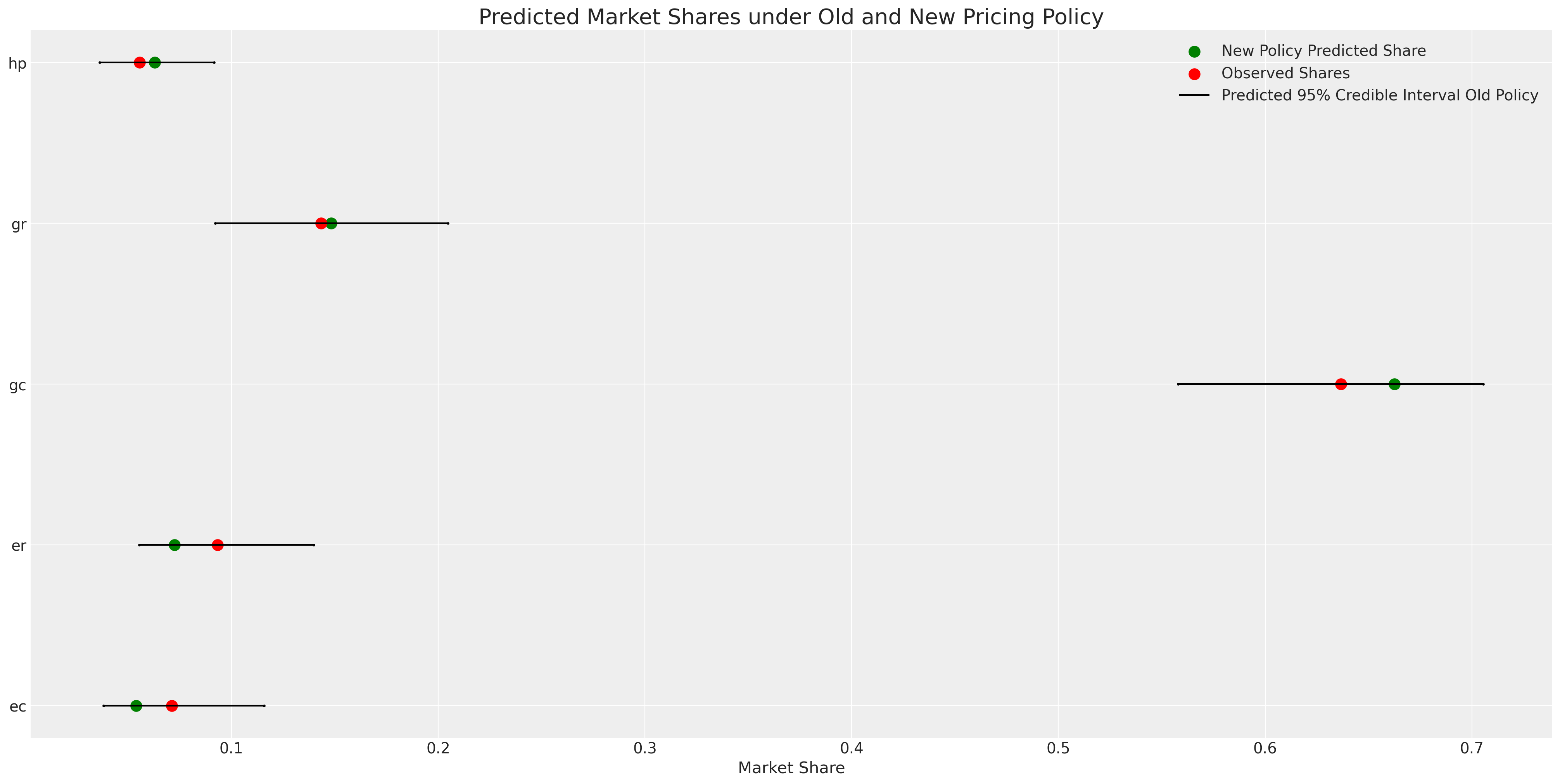

Model Adequacy and Counterfactuals

Pricing Experiments

Counterfactual Shares

Model Adequacy and Counterfactuals

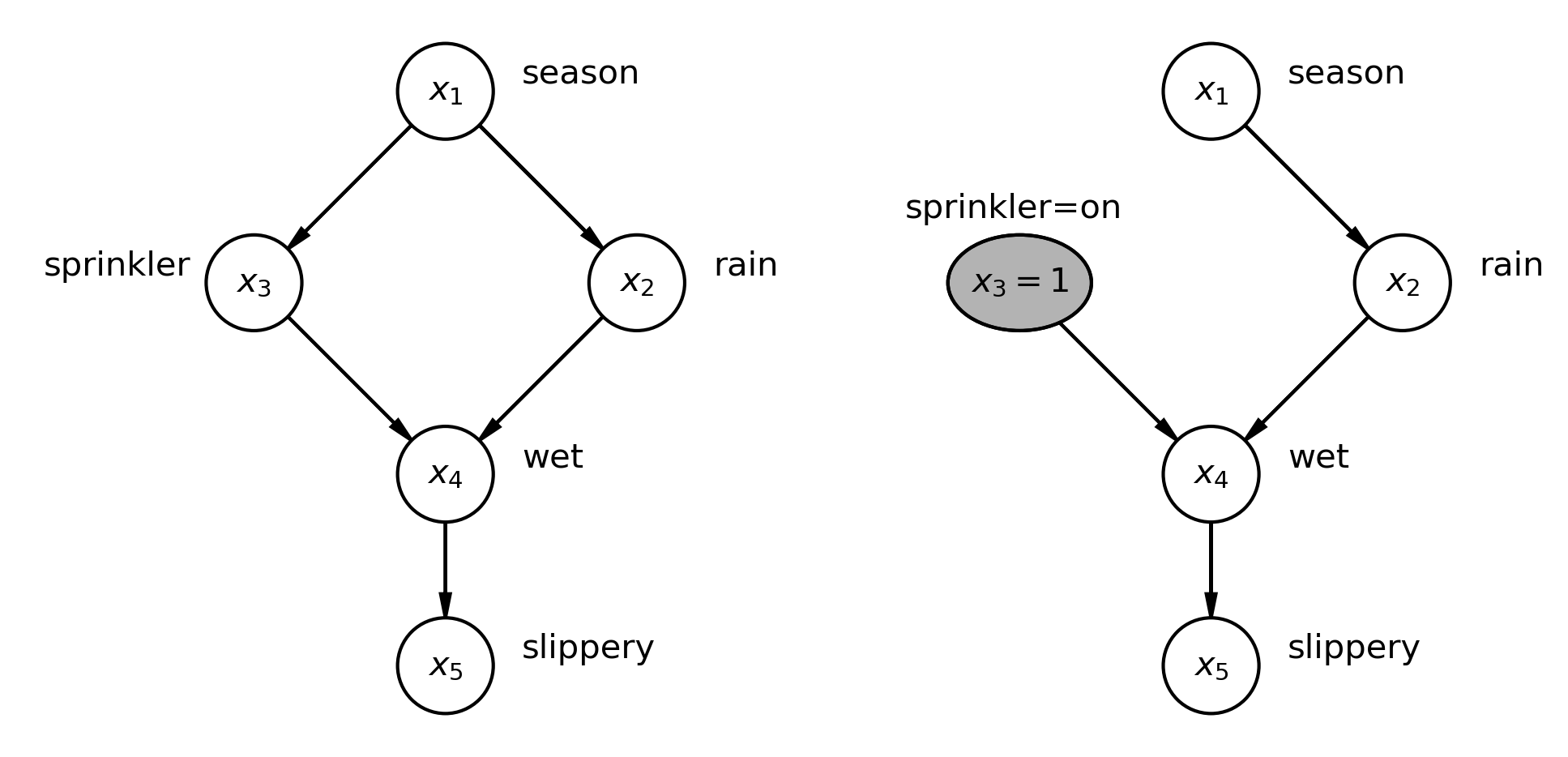

Interventions and Conditionalisation

- There is a sharp distinction between conditional probability distributions and probability under intervention

- In PyMC you can implement the do-operator to intervene on the graph that represents your data generating process.

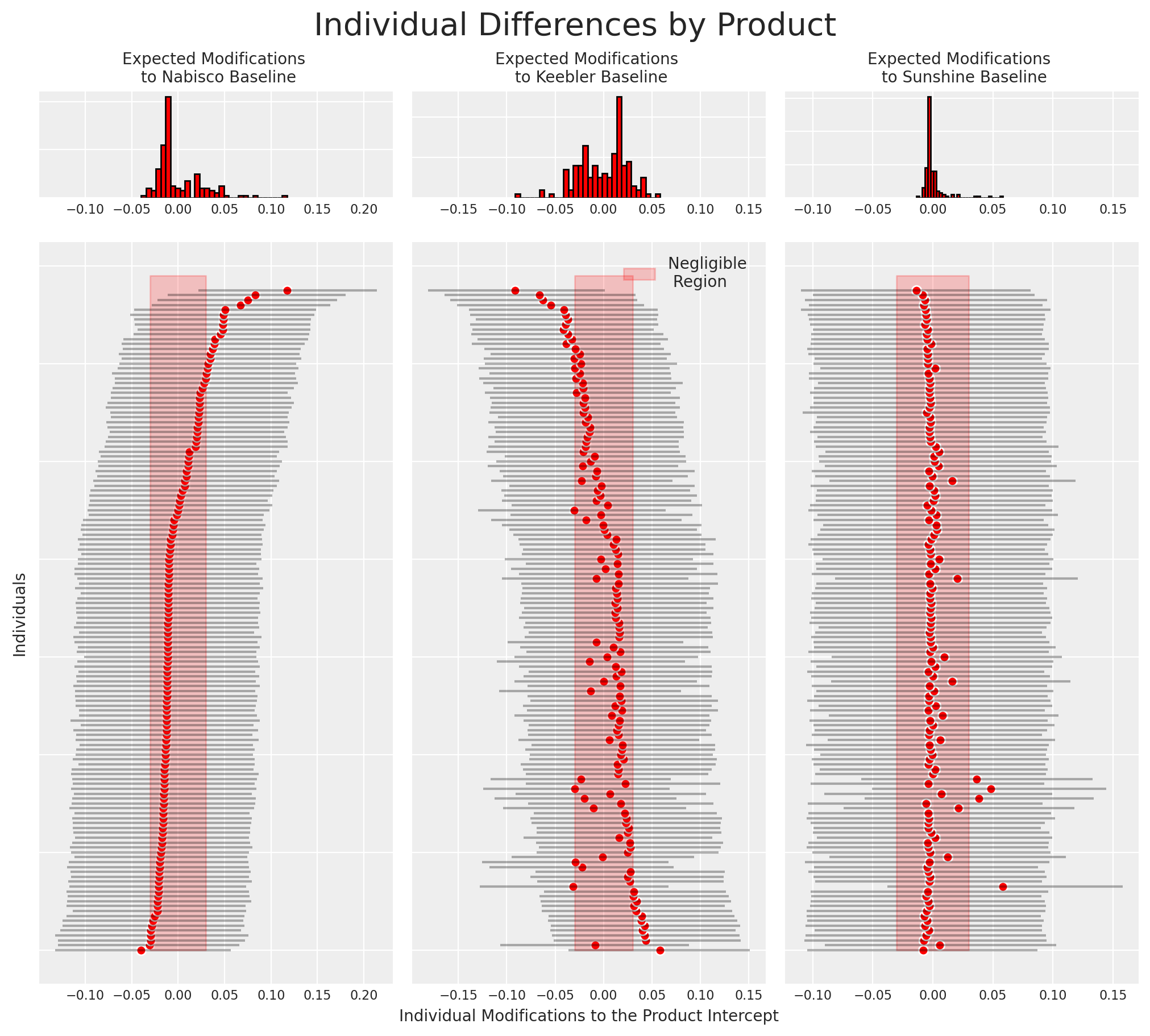

Individual Heterogenous Utility

Recovered Posterior Predictive Distribution

Individual Heterogenous Utility

Individual Preference

- Individual preferences can be derived from the model in this manner.

- The relationship between preferences over the product offering can be seen too

- Market stable under stable preferences?

Conclusion

The World in the Model

“Models… [are] like sonnets for the poet, [a] means to express accounts of life in exact, short form using languages that may easily abstract or analogise, and involve imaginative choices and even a certain degree of playfulness in expression” - Mary Morgan in The World in the Model

- Models should articulate the relevant structure of this world and other possible ones.

- They serve as microscopes. Simulation systems are tools to interrogate reality.

- Bayesian Conditionalisation calibrates the system against the observed facts.

- Bayesian Discrete choice models help us interrogate aspects of market demand under uncertainty.

- PyMC enables us to easily build and experiment with those models.

- Causal inference is plausible to degree that we can defend the structural assumptions. Bayesian models enforce tranparency and justification of structural commitments and necessary complexity.